Overview

Previous Year UPSC-CSE Questions By the end you will be able to draft model answers for the following UPSC questions. Each question carries a collapsible framework showing how to approach it in the exam.

- UPSC Mains 2016 GS-IIHas the Indian governmental system responded adequately to the demands of Liberalization, Privatization and Globalization started in 1991? What can the government do to be responsive to this important change?

How to structure the answer in the exam

Introduction: Open with 1991 changing the state's job description from gatekeeper to referee.

Body (sub-themes to develop):

- Adequate in part: statutory regulators (SEBI 1992, later telecom and insurance), competition law replacing MRTP, disinvestment machinery.

- Inadequate in part: slow administrative reform, persistence of discretionary controls, weak state capacity in agriculture and factor markets.

- What more: regulatory independence and accountability, process re-engineering and single-window governance, capacity building, cooperative centre-state economic governance.

- Anchor examples from the article: delicensing, the Narasimham banking reforms and the statutory regulators.

Conclusion: Conclude that the regulatory state arrived faster than the administrative state reformed, and closing that gap is the present agenda.

- UPSC Prelims 2017 GS Paper IWhich of the following has/have occurred in India after its liberalization of economic policies in 1991?

- Share of agriculture in GDP increased enormously.

- Share of India's exports in world trade increased.

- FDI inflows increased.

- India's foreign exchange reserves increased enormously.

Select the correct answer using the codes given below:

How to approach this Prelims question

Approach: Test each indicator against the post-1991 scoreboard; the agriculture statement is the designed error.

Trap to watch: Agriculture's GDP share falls in a growing economy; any option keeping statement 1 falls.

Key facts to recall:

- Exports' world share rose after 1991

- FDI inflows rose

- Reserves rose from a fortnight's cover to ample levels

- Agriculture's share of GDP kept declining

Answer signal: Statements 2, 3 and 4 only, so option (b).

- UPSC Prelims 1996 GS Paper IWhich one of the following is correct regarding stabilization and structural adjustment as two components of the new economic policy adopted in India?

How to approach this Prelims question

Approach: Map time horizons: stabilisation is the quick track, structural adjustment the gradual one.

Trap to watch: Option (a) swaps the two horizons; option (d) invents a centre-state division that does not exist.

Key facts to recall:

- Stabilisation: short-term, balance of payments and inflation

- Structural reform: long-term, efficiency and competitiveness

- Both are components of the same New Economic Policy

Answer signal: Structural adjustment gradual, stabilisation quick, so option (b).

- UPSC Prelims 2000 GS Paper IEconomic liberalisation in India started with

How to approach this Prelims question

Approach: Anchor liberalisation's first move to delicensing under the New Industrial Policy of 1991.

Trap to watch: Convertibility and tax reform came later in the reform sequence; they are consequences, not the starting point.

Key facts to recall:

- The New Industrial Policy dismantled licensing in 1991

- Devaluation and the July budget framed the turn

- Convertibility and tax reform followed in later steps

Answer signal: Substantial changes in industrial licensing policy, so option (a).

The 1991 economic reforms were born of an emergency: by mid-1991 India's foreign exchange reserves could not pay for even a fortnight of imports, and the government pledged national gold abroad to stay solvent. Out of that humiliation came the sharpest policy turn since independence, the New Economic Policy of liberalisation, privatisation and globalisation, the LPG reforms, and the dismantling of the licence raj this series described in the previous part, and the open economy India lives in today. This part follows the crisis, the rescue and the reckoning.

India in 1991: The Emergency That Reset the Economy

Why a Payments Crisis Became a Turning Point in Nation-Building

Why this matters: Every part of this series so far built towards a system, the planned, licensed, state-led economy. In 1991 that system met a creditor's deadline it could not meet, and the response rewrote the rules. The 1991 turn is therefore both an economic event and a chapter of political history.

What is the significance of the 1991 crisis: It is the hinge between the licence raj and the open economy. The crisis explains why reform came as a package and why it came so fast: stabilisation could not wait, and the lenders' conditionality made restructuring part of the price of rescue.

The Road to 1991: Twin Deficits, Borrowed Consumption and the Gulf Shock

How the 1980s Spent Their Way to the Brink

Distinguishing the causes: The origin of the crisis lay in the inefficient management of the economy through the 1980s. Government spending ran persistently ahead of revenue, and the gap was financed by borrowing, at home and abroad; imports grew far faster than exports, so the external gap widened alongside the fiscal one, the classic twin deficits.

Worse, foreign loans were at times spent on consumption rather than on capacity that could repay them, and little was done to boost exports to pay for the swelling imports. When the Gulf crisis of 1990 spiked oil prices and squeezed remittances, the cushion was already gone.

The Balance of Payments Emergency: Reserves Below a Fortnight of Imports

Debt Repayments, Rising Prices and the Threat of Default

Distinguishing the emergency: By 1991 the government was struggling to meet repayments on its foreign borrowings, and foreign exchange reserves, kept to pay for petroleum and other essential imports, dropped below what was needed to finance even a fortnight of imports. Rising prices of essential goods compounded the distress.

There was not enough foreign exchange even to service the interest owed to international lenders, and a sovereign default, never before suffered, became a live possibility. The crisis was no longer a statistic; it was a deadline.

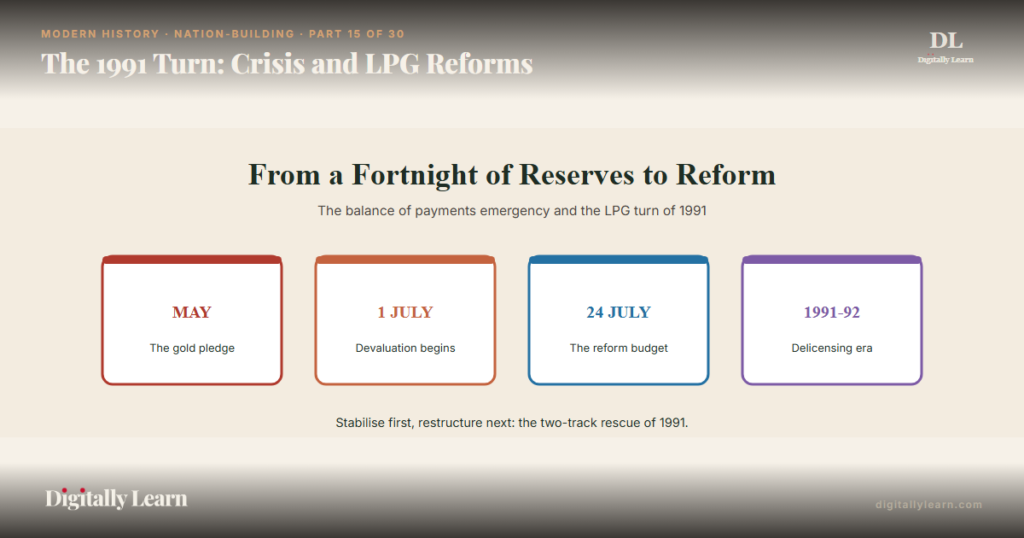

Pledging the Gold: The Airlift of May 1991 and the IMF Loan

Forty-Seven Tonnes to London, Twenty to Switzerland, and Seven Billion Dollars

Distinguishing the rescue: In May 1991, in conditions of secrecy amid a general election, the country pledged its gold: about 47 tonnes were airlifted to the Bank of England and about 20 tonnes went to the Union Bank of Switzerland, raising roughly 600 million dollars to keep payments flowing. The news, once out, caused public outrage and became the enduring symbol of the crisis.

Behind the gold stood the larger rescue: India approached the World Bank and the IMF and received about 7 billion dollars in loans. The lenders expected India to liberalise: open the economy, lift restrictions on private firms, narrow the state's role and ease trade barriers, the conditionality that shaped what followed.

The politics made the economics possible: The turn was carried by a minority government. Prime Minister P. V. Narasimha Rao, in office from June 1991 after a season of short-lived governments and a mid-election assassination had shaken the polity, gave his finance minister room to act and absorbed the political heat. Reform by quiet, steady steps rather than loud confrontation became the governing style, and it let a contested programme outlast its first parliament.

The New Economic Policy: Stabilisation Track and Structural Reform Track

Quick Repairs Versus Long Rebuilding: The Two Components Distinguished

Distinguishing the two tracks: The New Economic Policy ran on two timetables. Stabilisation measures were short-term and quick: repair the balance of payments and bring inflation under control, the firefighting of 1991-92. Structural reform measures were long-term and gradual, a multi-step rebuilding aimed at efficiency and international competitiveness by removing rigidities across the economy.

| Dimension | Stabilisation measures | Structural reform measures |

|---|---|---|

| Time horizon | Short-term, quick adaptation | Long-term, gradual and multi-step |

| Aim | Repair the balance of payments; control inflation | Efficiency and international competitiveness |

| Typical content | Reserves rebuilt, demand restrained, currency corrected | Delicensing, trade opening, financial and tax reform |

| Sequence | First, to stop the bleeding | Second, to rebuild the system |

The distinction is not pedantic; it is the architecture of the whole reform. Stabilisation bought time with the gold and the loan; structural reform spent that time dismantling the controls the previous part described, and the order could not have been reversed.

In the lenders' vocabulary the second track was the structural adjustment programme, the standard IMF and World Bank package of the era, which is why the period's policy vocabulary names stabilisation and structural adjustment as the two components of the New Economic Policy.

July 1991: Devaluation, the Reform Budget and the New Industrial Policy

Three Weeks That Ended the Licence Raj

Distinguishing the July moves: Reform arrived in steps days apart. On 1 July and 3 July 1991 the rupee was devalued in two instalments, by about nine and eleven per cent, to make exports competitive and signal the new course. On 24 July, finance minister Manmohan Singh presented the budget that formally announced the reform programme, with Prime Minister P. V. Narasimha Rao carrying the politics.

The same season's New Industrial Policy dismantled the licensing regime: the requirement of a government licence to start most private industry was abolished, the MRTP-era restraints on large houses were eased, public-sector reservation was narrowed, and foreign direct investment was welcomed into wide areas of industry. Liberalisation began, exactly as the old question form has it, with substantial changes in industrial licensing policy.

Just as telling is what 1991 left alone: the capital account was opened only gradually, and labour law and agricultural marketing were barely touched, the caution that kept the crisis response from becoming shock therapy.

- Devaluation: Two steps, 1 and 3 July 1991, roughly nine then eleven per cent.

- The budget of 24 July 1991: The formal announcement of the reform course.

- Delicensing: The licence requirement abolished for most industries.

- Opening: FDI welcomed, public-sector reservation narrowed, trade barriers lowered.

Liberalisation, Privatisation, Globalisation: What Each Pillar Actually Means

Two Strategies and One Outcome, with the Areas Each Reformed

Distinguishing the pillars: Liberalisation removed entry barriers and controls across industry, finance, taxation, foreign exchange and trade. Privatisation shrank the public sector's monopoly through disinvestment and private entry. Globalisation, properly understood, is not a third policy but the outcome of the first two: the integration of India's economy with the world economy.

The 1991 programme was more sweeping than anything before it, yet it had a prehistory: a few liberalising steps in licensing, export-import policy and technology had come in the 1980s, so 1991 made comprehensive what had been piecemeal. That is why the reforms read as a turn rather than an invention.

Liberalisation worked area by area: Industrial deregulation removed the licence gates; financial sector reform repositioned the RBI from controller towards regulator and admitted new private players; tax reform simplified and lowered rates to improve compliance; the foreign exchange market was deregulated step by step towards market-determined rates; and trade and investment reform cut tariffs, dismantled quantitative restrictions and eased the entry of foreign capital and technology.

Banking from Nationalisation to the Narasimham Reforms

Fourteen Banks in 1969, Six in 1980, and the 1991 Committee

Distinguishing the financial arc: The state had taken commanding control of banking a generation earlier: at midnight on 19 July 1969 the fourteen largest commercial banks were nationalised, and a second round in 1980 brought six more under state ownership. Branches spread into the countryside and credit was directed to priority sectors, but efficiency and profitability sagged under the same control logic as industry.

The purpose had been developmental: take banking from the cities to the villages, direct credit to priority sectors such as agriculture and small industry, and put household savings behind the plan, and on branch spread and deposit growth the policy delivered.

The reform era answered with the Narasimham Committee of 1991, which charted financial sector reform: prudential norms, competition, and the entry of new private banks. Banking thus traces the whole arc of this series in miniature, state capture for development goals, then market discipline to repair the costs.

Assessing the Reforms: What Rose, What Lagged and Who Was Left Out

Exports, FDI and Reserves Up; Agriculture and Industry Under Strain

Observable outcomes after 1991 are now settled facts: India's share of world exports rose, FDI inflows rose, and foreign exchange reserves rose from a fortnight's cover to among the world's largest holdings. The share of agriculture in GDP did not rise; it continued its long structural decline as services surged.

The appraisal is genuinely two-sided. Growth quickened and the consumer economy widened, but the boom concentrated in services, telecommunication, information technology, finance and trade, while agriculture saw public investment fall and industry faced cheaper imports with lower investment.

Membership of the World Trade Organization from its founding in 1995 then locked the open trade regime into treaty, a thread the capstone part follows. Critics add that inequality widened between groups and regions, the debate the capstone part of this series returns to.

The sharpest critics go further: the externally advised package, they argue, deepened existing inequalities, lifted the consumption of higher-income groups first, and concentrated growth in a few service sectors and regions rather than in the fields and factories where most Indians earn, an argument the reform's defenders answer with the poverty decline of the high-growth years.

| Indicator | Direction after 1991 | Reading |

|---|---|---|

| Share of world exports | Rose | Openness worked for trade |

| FDI inflows | Rose | Investor confidence returned |

| Foreign exchange reserves | Rose strongly | From a fortnight's cover to ample cushions |

| Agriculture's share of GDP | Did not rise; kept declining | Structural shift, and a sector left behind |

| Services | Surged | The new engine of growth |

Did Government Itself Keep Pace with Liberalisation?

The governance question follows naturally: An economy freed from licensing still needed the state, but a different one, a referee rather than a gatekeeper. The answer came piecemeal: regulators such as SEBI for securities markets were given statutory teeth in 1992, and sector regulators followed in telecom, insurance and beyond, while administrative reform of the old permission-issuing machinery moved far more slowly.

The honest assessment is therefore mixed: the state re-equipped itself for markets in finance and infrastructure faster than it reformed its own administration, and the gap between a liberalised economy and a pre-reform bureaucracy remains a live governance theme.

Significance: 1991 as the Second Founding of the Indian Economy

Why the Crisis Year Remains the Reference Point for All Economic Policy

The larger significance of 1991 is that it functions as a second founding: the moment the republic chose openness under duress and then kept it by choice. Every later reform argues from 1991, and every backslide is measured against it. The gold pledge gave the turn its emotional charge; the conditionality gave it its content.

Contemporary linkages keep the year current: foreign exchange reserves are now reported as strength rather than survival, trade policy debates assume an open economy, and the unfinished items of 1991, factor markets, administrative reform, agriculture, remain the present agenda. The next part leaves economics for the world stage, the foundations of India's foreign policy.

- Twin deficits, borrowed consumption and the Gulf shock drove reserves below a fortnight of imports.

- India pledged about 47 tonnes of gold to the Bank of England and 20 to UBS, and borrowed about 7 billion dollars.

- Devaluation came in two steps on 1 and 3 July 1991; the 24 July budget announced the reform course.

- The New Industrial Policy dismantled licensing; liberalisation and privatisation were strategies, globalisation the outcome.

- Exports, FDI and reserves rose after 1991, while agriculture and parts of industry lagged.

Prelims MCQ practice

Each question below tests one specific concept on the topic. Click to reveal the answer and a full option-wise explanation.

Q1. Consider the following statements about the gold pledge of 1991:

- About 47 tonnes of gold were airlifted to the Bank of England.

- About 20 tonnes of gold went to the Union Bank of Switzerland.

- The pledges raised roughly 600 million dollars.

Which of the statements given above are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1, 2 and 3

Explanation.

All three statements are correct. In May 1991 about 47 tonnes of gold were airlifted to the Bank of England and about 20 tonnes went to the Union Bank of Switzerland, together raising roughly 600 million dollars. Hence option (d).

Q2. In July 1991 the rupee was devalued in two steps. On which dates did the two steps fall?

- 1 and 3 July

- 10 and 12 July

- 24 and 26 July

- 30 and 31 July

Show answer and explanation

Answer: 1 and 3 July

Explanation.

Option (a) is correct. The rupee was devalued on 1 July and again on 3 July 1991, by roughly nine and eleven per cent, ahead of the 24 July reform budget. Hence option (a).

Q3. Consider the following statements about the nationalisation of banks in India:

- Fourteen of the largest commercial banks were nationalised in 1969.

- A second round in 1980 nationalised six more banks.

- The Narasimham Committee of 1991 recommended financial sector reform.

Which of the statements given above are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1, 2 and 3

Explanation.

All three statements are correct: fourteen banks were nationalised with effect from 19 July 1969, six more followed in 1980, and the Narasimham Committee of 1991 charted the post-reform financial sector. Hence option (d).

Q4. Under the New Economic Policy of 1991, which component was designed as the short-term, quick track?

- Structural reform measures

- Stabilisation measures

- Privatisation of state enterprises

- Globalisation of trade

Show answer and explanation

Answer: Stabilisation measures

Explanation.

Option (b) is correct. Stabilisation measures were the short-term track, repairing the balance of payments and controlling inflation, while structural reform was the gradual long-term rebuilding. Hence option (b).

Q5. Consider the following statements about liberalisation, privatisation and globalisation:

- Liberalisation and privatisation are policy strategies.

- Globalisation is best understood as the outcome of those strategies.

- Globalisation was a third, independent policy unconnected to the other two.

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1 and 2 only

Explanation.

Statements 1 and 2 are correct: liberalisation and privatisation are the strategies and globalisation, the integration of the economy with the world economy, is their outcome. Statement 3 contradicts that relationship. Hence option (b).

Q6. Approximately how large was the loan India received from the World Bank and the IMF to manage the 1991 crisis?

- 1 billion dollars

- 3 billion dollars

- 7 billion dollars

- 15 billion dollars

Show answer and explanation

Answer: 7 billion dollars

Explanation.

Option (c) is correct. India received about 7 billion dollars as loan from the World Bank and the IMF, against the expectation that it would liberalise and open up the economy. Hence option (c).

Sources and Further Reading

- NCERT, Indian Economic Development (Class 11), Liberalisation, Privatisation and Globalisation: An Appraisal

- Wikipedia: 1991 Indian economic crisis

- Wikipedia: Economic liberalisation in India

- Wikipedia: Banking in India

- Reserve Bank of India

- Department of Investment and Public Asset Management (DIPAM)

- Press Information Bureau, Government of India

- National Portal of India

Editorial Disclaimer

This article is prepared for UPSC examination preparation. Verify key facts and interpretations against standard reference histories before relying on them.