Overview

Previous Year UPSC-CSE Questions By the end you will be able to draft model answers for the following UPSC questions. Each question carries a collapsible framework showing how to approach it in the exam.

- UPSC Prelims 2015With reference to the Fourteenth Finance Commission, consider the following statements:

- It increased the share of States in the central divisible pool from 32 per cent to 42 per cent.

- It made recommendations concerning sector-specific grants.

Which of the statements given above is/are correct?

How to approach this Prelims question

Approach: Check each statement against what the 14th Commission actually did.

Trap to watch: Statement 2 is the trap: the 14th Commission moved away from sector-specific grants, giving States more untied funds, so it did not recommend sector-specific grants.

Key facts to recall:

- The 14th Finance Commission raised the vertical share from 32 to 42 per cent.

- It deliberately avoided sector-specific grants, favouring untied devolution.

- The 15th and 16th Commissions set the share at 41 per cent.

Answer signal: Statement 1 is correct; statement 2 is incorrect. Correct answer: 1 only.

- UPSC Mains 2018 GS-IIHow is the Finance Commission of India constituted? What do you know about the terms of reference of the recently constituted Finance Commission? Discuss.

How to structure the answer in the exam

Introduction: Open with Article 280: the Finance Commission as a constitutional body set up every five years to recommend Centre-State revenue sharing.

Body (sub-themes to develop):

- Constitution: appointed by the President; a chairperson and four members; qualifications set by Parliament.

- Core terms of reference: distribution of net tax proceeds (vertical) and the inter-State formula (horizontal).

- Grants-in-aid, including revenue-deficit, local-body and disaster-management grants.

- The 16th Commission's award for 2026-31 retained the 41 per cent vertical share.

- Debates: cesses and surcharges outside the divisible pool, and population-based horizontal criteria.

Conclusion: Conclude that the Commission is the institutional anchor of fiscal federalism, balancing Union priorities with State autonomy.

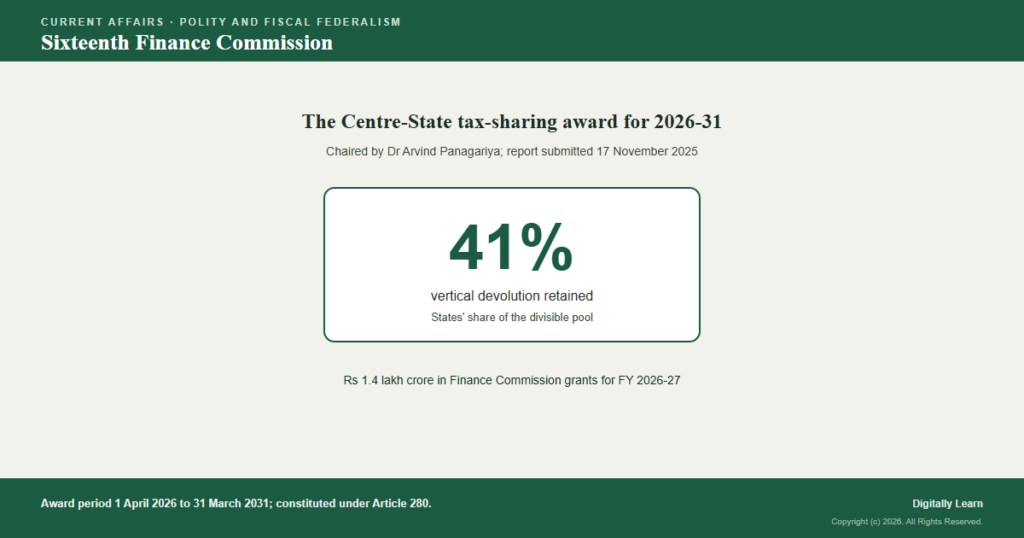

The Finance Commission is a constitutional body set up under Article 280 every five years to recommend how tax revenue is shared between the Union and the States. The Sixteenth Finance Commission, chaired by Dr Arvind Panagariya, submitted its report for the 2026-31 award period to the President on 17 November 2025; the government accepted retaining the 41 per cent vertical devolution share in the Union Budget 2026-27, with the award commencing on 1 April 2026.

Why the Sixteenth Finance Commission is in focus

From report submission to the 2026-31 award

The award of the Sixteenth Finance Commission covers the five years from 1 April 2026 to 31 March 2031. The Commission, chaired by Dr Arvind Panagariya, submitted its report to the President on 17 November 2025.

The Finance Commission is a constitutional body under Article 280, set up roughly every five years. It recommends how the net proceeds of central taxes are shared with the States and how grants-in-aid are distributed, giving States a predictable resource framework.

The government accepted the Commission's recommendation to retain the vertical devolution share at 41 per cent, announced while presenting the Union Budget 2026-27. The report is then laid in Parliament with an explanatory memorandum on the action taken, as required by Article 281.

The headline elements of the award are:

- Vertical devolution: the States’ share of the divisible pool of central taxes retained at 41 per cent.

- Grants: Rs 1.4 lakh crore in Finance Commission grants for FY 2026-27, including rural and urban local-body grants and disaster-management grants.

- Award period: five years, 2026-27 to 2030-31, commencing 1 April 2026.

- Mandate: tax-sharing, grants-in-aid, support to local bodies, and financing of disaster management.

Why the award matters for the States

The backbone of Centre-State fiscal relations

The Finance Commission's award is the single largest determinant of how much untied money the States receive. State budgets, welfare spending and capital plans for five years are built on its devolution share and grants.

Retaining the share at 41 per cent keeps the settlement broadly stable. It avoids a sharp swing in States' resources at a time when they carry large spending responsibilities in health, education and capital works.

Stability also matters for predictability. Because the award runs for five years, a steady vertical share lets State governments plan medium-term borrowing and expenditure without a mid-cycle shock to their tax transfers.

What retaining the 41 per cent share signifies

Continuity, grants and the divisible-pool question

Three threads carry the weight: continuity in the devolution share, the grant architecture, and the longer-running debate over the size of the divisible pool itself.

First, continuity. Holding the share at 41 per cent signals that the Centre and the Commission judged the existing balance broadly appropriate, rather than reopening the vertical split that the 14th Commission had raised to 42 per cent.

Second, the grants. The Rs 1.4 lakh crore for FY 2026-27 flows partly to rural and urban local bodies and to disaster management, channelling money to the third tier of government and to resilience, not only to State treasuries.

Third, the divisible-pool debate. States have long argued that cesses and surcharges, which sit outside the divisible pool, shrink what is actually shared. A 41 per cent share of a pool that excludes those levies is the structural concern that endures beyond any single award.

Distinguishing features of the Finance Commission settlement

The devolution share across recent Commissions

The table places the 16th Commission's vertical share against its recent predecessors, so the trajectory of Centre-State tax sharing is visible at a glance.

| Finance Commission | Award period | Vertical devolution share |

|---|---|---|

| 13th Finance Commission | 2010-15 | 32 per cent |

| 14th Finance Commission | 2015-20 | 42 per cent |

| 15th Finance Commission | 2021-26 | 41 per cent |

| 16th Finance Commission | 2026-31 | 41 per cent (retained) |

Three features that define the award

Three elements define how the Commission's award works:

- (i) Vertical devolution. The division of central taxes between the Union and the States as a whole, retained at 41 per cent of the divisible pool for 2026-31.

- (ii) Horizontal devolution. The formula that splits the States’ share among individual States, using criteria such as population, area, income distance, demographic performance and forest cover.

- (iii) Grants-in-aid. Transfers beyond the tax share, including revenue-deficit grants, local-body grants and disaster-management grants under the award.

Observable outcomes of the 2026-31 award

Three trackable outcomes

The award translates into three visible outcomes over the coming five years.

- (a) Tax transfers to States at the 41 per cent vertical share through the divisible pool, beginning with FY 2026-27.

- (b) Rs 1.4 lakh crore in grants for FY 2026-27, flowing to local bodies and disaster-management funds alongside the tax share.

- (c) Parliamentary scrutiny, as the report and the action-taken report are laid before Parliament under Article 281.

The headline 41 per cent applies to the divisible pool, which excludes cesses and surcharges. The effective transfer to States therefore depends on how large that pool is, not on the percentage alone.

India's fiscal-federalism debates

Cesses, GST and the federal balance

The award sits inside a wider fiscal-federalism debate. The most persistent issue is the rise of cesses and surcharges, which the Union retains outside the divisible pool, reducing the base on which the 41 per cent is applied.

It connects to the Goods and Services Tax settlement, where States ceded taxing powers in exchange for a share of a common pool, sharpening their reliance on transfers. Several southern States have also raised concerns that population-weighted formulas can penalise success in controlling fertility.

The award reinforces the language of cooperative and competitive federalism. A stable devolution share, paired with performance-linked grants, is the lever through which the Centre nudges State behaviour while protecting their fiscal autonomy.

UPSC relevance and exam focus

Where this fits in the UPSC-CSE syllabus

This topic maps to General Studies Paper II: functions and responsibilities of the Union and the States, and issues in the federal structure, and to General Studies Paper III: mobilisation of resources and government budgeting.

For Prelims, hold the high-yield facts: the constitutional basis (Article 280), the laying of the report (Article 281), the chairperson (Arvind Panagariya), the award period (2026-31), the vertical share retained (41 per cent), and the grant figure (Rs 1.4 lakh crore for FY 2026-27).

For Mains, two framings recur: how the Finance Commission balances vertical and horizontal devolution, and how the growth of cesses and surcharges outside the divisible pool affects genuine fiscal federalism.

Recurring linked concepts an aspirant should keep in working memory:

- Article 280: constitution of the Finance Commission every five years.

- Vertical vs horizontal devolution: Union-States split, then the inter-State split by formula.

- Divisible pool: the shareable taxes, excluding cesses and surcharges.

- Recent shares: 13th FC 32 per cent, 14th FC 42 per cent, 15th and 16th FC 41 per cent.

The Finance Commission is constituted under Article 280, and the President lays its report before Parliament under Article 281. Confusing these two articles is a frequent error.

Do not equate a 41 per cent share with 41 per cent of all central taxes. The share applies only to the divisible pool, which excludes cesses and surcharges, so the effective transfer is lower.

Prelims MCQ practice

Each question below tests one specific concept on the topic. Click to reveal the answer and a full option-wise explanation.

Q1. Consider the following statements regarding the Sixteenth Finance Commission:

- It was constituted under Article 280 of the Constitution.

- Its award covers the period 2026-27 to 2030-31.

- The government accepted retaining the vertical devolution share at 41 per cent.

Which of the statements given above is/are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1, 2 and 3

Explanation.

All three are correct. The Finance Commission is constituted under Article 280; the 16th Commission's award runs 2026-27 to 2030-31; and the government accepted retaining the vertical share at 41 per cent. Hence 1, 2 and 3.

Q2. Consider the following statements about devolution under the Finance Commission:

- Vertical devolution divides taxes between the Union and the States as a whole.

- The 41 per cent share applies to all central taxes, including cesses and surcharges.

- Horizontal devolution distributes the States' share among individual States by a formula.

Which of the statements given above is/are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1 and 3 only

Explanation.

Statements 1 and 3 are correct definitions of vertical and horizontal devolution. Statement 2 is incorrect: the 41 per cent applies to the divisible pool, which excludes cesses and surcharges. Hence 1 and 3 only.

Q3. Under which Article of the Constitution does the President cause the Finance Commission's report and the action-taken memorandum to be laid before Parliament?

- Article 280

- Article 281

- Article 275

- Article 282

Show answer and explanation

Answer: Article 281

Explanation.

Article 281 requires the President to lay the Finance Commission's report, with an explanatory memorandum on the action taken, before each House of Parliament. Article 280 constitutes the Commission; Article 275 covers statutory grants-in-aid; Article 282 covers discretionary grants. Hence option (b).

Q4. Consider the following statements regarding the 16th Finance Commission's award:

- It was chaired by Dr Arvind Panagariya.

- The report was submitted to the President in November 2025.

- It provided Rs 1.4 lakh crore in Finance Commission grants for FY 2026-27.

Which of the statements given above is/are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1, 2 and 3

Explanation.

All three are correct. Dr Arvind Panagariya chaired the 16th Commission; the report was submitted to the President in November 2025; and the award provides Rs 1.4 lakh crore in Finance Commission grants for FY 2026-27. Hence 1, 2 and 3.

Q5. Which one of the following is NOT among the standard criteria used by recent Finance Commissions for horizontal devolution among States?

- Income distance

- Demographic performance

- Forest and ecology

- Defence expenditure of the State

Show answer and explanation

Answer: Defence expenditure of the State

Explanation.

Income distance, demographic performance, and forest and ecology are standard horizontal-devolution criteria, along with population and area. Defence is a Union subject and State defence expenditure is not a devolution criterion. Hence option (d).

Q6. Across recent Finance Commissions, the vertical devolution share to States moved in which one of the following sequences?

- 32% (13th) to 42% (14th) to 41% (15th) to 41% (16th)

- 42% (13th) to 32% (14th) to 41% (15th) to 41% (16th)

- 41% (13th) to 41% (14th) to 42% (15th) to 32% (16th)

- 32% (13th) to 41% (14th) to 42% (15th) to 41% (16th)

Show answer and explanation

Answer: 32% (13th) to 42% (14th) to 41% (15th) to 41% (16th)

Explanation.

The 13th Commission set 32 per cent, the 14th raised it sharply to 42 per cent, the 15th trimmed it to 41 per cent, and the 16th retained 41 per cent. Hence option (a).

Sources and Further Reading

- Finance Commission of India: official site and 16th FC reports

- Press Information Bureau: 16th Finance Commission submits its report for 2026-31 to the President

- Press Information Bureau: Government accepts retaining vertical devolution at 41 per cent

- Press Information Bureau: Government constitutes the 16th Finance Commission with Dr Arvind Panagariya as Chairman

- Ministry of Finance: Department of Expenditure

- Wikipedia: Sixteenth Finance Commission

Editorial Disclaimer

This article is compiled from the reference materials listed in the Sources section. It is an explainer for UPSC preparation and is not a substitute for primary documents (NCERTs, GoI ministry releases, IMD bulletins, RBI / CEA / MoEFCC publications, and Standing-Committee reports).