Overview

RBI Defends the Currency

The rupee touched about 96.96 per US dollar on 20 May 2026 as the RBI sold dollars to keep the fall orderly.

Previous Year UPSC-CSE Questions By the end you will be able to draft model answers for the following UPSC questions. Each question carries a collapsible framework showing how to approach it in the exam.

- UPSC Mains 2018 GS-IIIHow would the recent phenomena of protectionism and currency manipulations in world trade affect macroeconomic stability of India?

How to structure the answer in the exam

Introduction: Open with the post-2017 protectionism wave (US tariff regimes, reciprocal-tariff thresholds), name currency-manipulation labels as the parallel pressure track, and frame the impact assessment through four macroeconomic channels.

Body (sub-themes to develop):

- Export channel: Indian goods exports under US reciprocal tariffs face a narrowing trade surplus; key sectors affected include textiles, gems and jewellery, leather, marine products, and pharmaceuticals. The 2026 widening trade deficit reflects the cumulative tariff load.

- Current account channel: the goods-trade deficit at the binding constraint widens the current account deficit beyond 2 per cent of GDP in 2026; remittances and services exports partially offset.

- Exchange rate channel: rupee depreciation to a record low near 96.96 per USD on 20 May 2026; 7.04 per cent year-to-date depreciation; the RBI Governor Sanjay Malhotra's orderly-market intervention framing.

- Capital flow channel: FPI outflows of over 22 billion US dollars in 2026 from Indian equity and debt markets; the narrowed US-India interest-rate differential reduces carry-trade attractiveness.

- Government and RBI response stack: India-EU FTA negotiation, services-export deepening, Foreign Trade Policy 2023 incentives; RBI three-layer rupee-defence toolkit (intervention, liquidity, monetary-policy layers); forex reserves near 681 billion US dollars as buffer, with the Governor citing about 700 billion US dollars of available resources.

Conclusion: Conclude that protectionism and currency-manipulation pressures transmit to Indian macroeconomic stability through four channels (exports, current account, exchange rate, capital flows), that the May 2026 rupee episode is the most current empirical evidence, and that the RBI three-layer policy stack and the diversification of trade partnerships are the operative response surface.

The May 2026 rupee fall to a record low near 96.96 per USD is the most-current empirical evidence of how the US tariff-and-protectionism channel transmits to Indian macroeconomic stability. The body sub-theme on exchange-rate channel supplies the leading 2026 evidence pillar.

- UPSC Mains 2015 GS-IIICraze for gold in India has led to a surge in the import of gold in recent years and put pressure on balance of payments and external value of the rupee. In view of this, examine the merits of the Gold Monetization scheme.

How to structure the answer in the exam

Introduction: Open with India as the world's second-largest gold consumer and gold imports as approximately 8-10 per cent of total goods imports, name the November 2015 launch of the Gold Monetization Scheme, and structure the answer through merit-and-limit buckets.

Body (sub-themes to develop):

- Gold Monetization Scheme (GMS) architecture: Short Term Bank Deposit (1-3 years), Medium Term Government Deposit (5-7 years), Long Term Government Deposit (12-15 years); rebate interest rates of 2.25 per cent to 2.50 per cent; conducted via authorised collection-and-purity-testing centres (CPTCs) and banks.

- Merit 1: Balance-of-payments support; recycling household gold reduces import-side foreign-exchange outflow on bullion; relevant in the May 2026 rupee context where the goods-trade deficit is the binding constraint.

- Merit 2: Household-gold mobilisation; approximately 24,000-25,000 tonnes of household and temple gold exists in India; even 10 per cent mobilisation eases import demand.

- Merit 3: Export-conversion; recycled gold supplied to gem-and-jewellery exporters under the GMS reduces fresh-import need.

- Limits and fiscal cost: incentive interest costs to the exchequer; low uptake against the household stock; cultural-and-trust barriers to depositing inherited gold; the Sovereign Gold Bond (SGB) scheme of 2015 acts as a complementary financial-asset substitute.

Conclusion: Conclude that the Gold Monetization Scheme has merit on balance-of-payments support, household-gold mobilisation, and export-conversion fronts, that uptake has been below potential against the 24,000-25,000-tonne stock, and that the May 2026 rupee depreciation reaffirms the relevance of the scheme alongside the Sovereign Gold Bond and Foreign Trade Policy 2023 measures.

The May 2026 rupee depreciation reaffirms the relevance of the 2015 question on balance-of-payments pressure from gold imports. The body sub-theme on Merit-1 BoP support supplies the leading 2026-current evidence pillar.

Currency depreciation is the fall in the external value of a country's currency against another country's currency in a floating or managed-floating exchange-rate regime. Rupee depreciation refers to a fall in the external value of the Indian Rupee (INR) against the US Dollar (USD) or against a basket of currencies measured by the Real Effective Exchange Rate (REER) tracked by the Reserve Bank of India. On 20 May 2026, the rupee touched a record low of about 96.96 per US dollar in intraday trade.

Why this is in the news on 22 May 2026

The all-time low and the RBI intervention

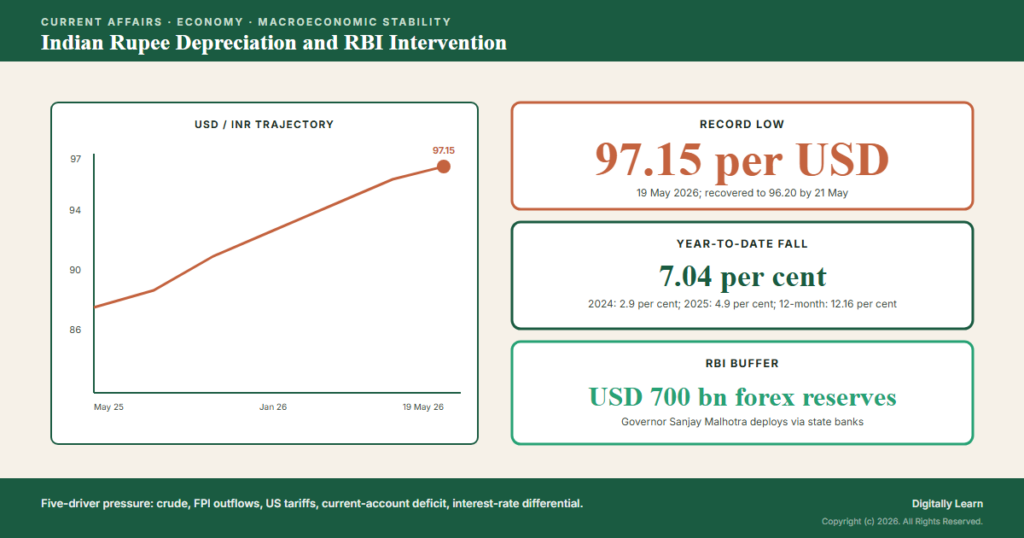

On 20 May 2026, the Indian rupee touched a record low of about 96.96 against the US dollar in intraday trade on the spot market, breaching its previous record low of roughly 96.61 from the prior session. The Reserve Bank of India (RBI) intervened heavily through state-run banks, which limited the slide and brought the rupee to a record closing low of 96.82.

Definition: Currency depreciation is the fall in the external value of a country's currency against another country's currency in a floating or managed-floating exchange-rate regime. India operates a managed-float regime in which the RBI intervenes to smooth volatility without targeting a specific exchange rate level.

Three data points define the May 2026 episode:

- (i) Record low. An intraday low near 96.96 per USD on 20 May 2026 and a record closing low of 96.82, surpassing the previous record. RBI dollar sales through state-run banks limited the slide.

- (ii) Year-to-date depreciation. 7.04 per cent in the first five months of 2026, against full-year 4.9 per cent in 2025 and 2.9 per cent in 2024. The trailing-12-month depreciation is about 12 per cent.

- (iii) RBI policy posture. Governor Sanjay Malhotra stated that the central bank would do whatever is required to ensure orderly price discovery in the forex market, citing about 700 billion US dollars in foreign-exchange reserves as the available buffer, against a reserves level near 681 billion US dollars by the week ending 22 May 2026.

Why the depreciation matters for macroeconomic stability

The five pressure channels driving the rupee fall

Why it matters: The 2026 rupee episode matters because the year-to-date fall of 7.04 per cent in five months already exceeds the full-year decline in both 2024 and 2025, marking the steepest pace since the 2013 taper-tantrum episode. Five pressure channels are simultaneously active, which means the depreciation reflects a structural and cyclical convergence rather than a single shock.

The May 2026 episode also matters because it brought the rupee back into RBI policy discourse. Governor Sanjay Malhotra's remark that the rupee has become undervalued, in both nominal and real-effective-exchange-rate terms, signals the RBI's reading that the depreciation has overshot fundamentals. The remark frames the central bank's intervention through a fair-value lens, while the RBI reiterates that it does not target a specific exchange-rate level.

Significance for macroeconomic policy

What the depreciation means for inflation, external debt, and trade competitiveness

What is the significance of this issue: The May 2026 depreciation episode carries three significances for macroeconomic policy:

- (i) Imported-inflation transmission. The pass-through from a depreciating rupee to wholesale-price inflation is concentrated in crude oil, fertilisers, electronics, and edible oils. With CPI inflation back within the 4 per cent (+/- 2) RBI target band, a sustained 10 per cent depreciation can add 30-50 basis points to headline inflation.

- (ii) External-debt-servicing cost. India’s external debt stood at approximately 765 billion US dollars as of end-2025. A 7 per cent rupee fall raises the rupee-denominated cost of external-debt servicing for Indian sovereigns and corporates with USD liabilities.

- (iii) Trade-competitiveness vs financial-stability trade-off. A weaker rupee supports goods and IT-services exports under a depressed-export-prices channel, but a disorderly depreciation undermines financial stability by triggering further FPI outflows and one-way bets. The RBI’s choice of orderly as the operative adjective frames the trade-off.

Distinguishing features of the RBI intervention toolkit

The RBI's three-layer rupee-defence toolkit

Distinguishing features: The RBI deploys three policy levers for orderly market intervention:

- (i) Spot-and-forward dollar sales. The RBI sells US dollars from its forex reserves through state-run banks in the spot, forward, and non-deliverable forward (NDF) markets. The intervention smooths volatility without targeting a specific exchange rate level.

- (ii) Currency swaps and overseas dollar raising. The RBI conducts USD-INR sell-buy swaps with banks to manage rupee liquidity while injecting dollar supply. It can also raise dollars from overseas investors via Foreign Currency Non-Resident Bank (FCNR-B) deposit incentives or NRI-bond issuance.

- (iii) Policy-rate signalling. Marginal increases in the repo rate or in the cash reserve ratio (CRR) shift the interest-rate differential and reduce one-way depreciation bets. The RBI Governor’s orderly market remark is itself a verbal-intervention lever that reduces speculative positioning.

The May 2026 rupee episode in numbers

| Indicator | Detail | Significance |

|---|---|---|

| Record intraday low | About 96.96 per USD on 20 May 2026 | Record low in intraday trade |

| Record closing low | 96.82 per USD on 20 May 2026 | Post-RBI intervention close |

| Year-to-date depreciation | 7.04 per cent (Jan-May 2026) | Highest annual pace since 2013 taper tantrum |

| Trailing-12-month fall | About 12 per cent | Steepest annual fall in over a decade |

| Forex reserves | Near 681 billion US dollars (week ending 22 May 2026) | Buffer drawn down by intervention from above 700 billion in 2025 |

| RBI Governor | Sanjay Malhotra | Stated the rupee has become undervalued |

| Inflation pass-through | 30-50 basis points per 10 per cent fall | Concentrated in crude, fertilisers, electronics |

| External debt | Approximately 765 billion US dollars (end-2025) | Rupee-denominated servicing cost rises |

| FPI outflows | Over 22 billion US dollars in 2026 | Equity and debt outflows |

| Crude-oil import share | Approximately 85 per cent of consumption | Iran war price spike transmitted |

Observable outcomes to track through 2026-27

What to watch on the rupee and the RBI policy stack through 2026-27

Observable outcomes: Six outcomes frame the rupee trajectory and the macro-policy response over 2026-27:

- (a) Forex-reserves trajectory. Whether reserves remain above the 600 billion US dollar floor or draw down materially under sustained intervention.

- (b) Real Effective Exchange Rate (REER). Whether the 40-currency trade-weighted REER, calculated by RBI, signals further overvaluation or returns toward the equilibrium band.

- (c) Current account deficit. Whether the CAD widens beyond 2 per cent of GDP or compresses through services-export and remittances strength.

- (d) FPI flows. Whether the equity and debt outflows reverse on RBI policy clarity or on global-risk-off conditions stabilising.

- (e) Monetary Policy Committee stance. Whether the MPC pivots from neutral to hawkish on the next review or holds the repo rate at the current level.

- (f) Imported-inflation pass-through. Whether headline CPI inflation breaches the 4 per cent (+/- 2) RBI target band on imported-inflation transmission.

Threads connecting the rupee to wider external-sector policy

How the rupee episode connects to protectionism, the BoP, and the inflation-targeting mandate

Contemporary linkages: Three threads connect the May 2026 rupee episode to wider external-sector policy.

The first is the protectionism-and-currency-manipulation thread. The 2018 GS-III Mains question on protectionism and currency manipulation maps directly onto the 2026 US-tariff-pressure channel. The Indian response runs through diversification of export destinations, services-export deepening, and the India-EU FTA negotiation.

The second is the balance-of-payments-and-gold thread. The 2015 GS-III Mains question on gold imports and the external value of the rupee remains live; India is the world's second-largest gold consumer and gold imports contribute to the goods-trade deficit. The Gold Monetization Scheme (2015) and the Sovereign Gold Bond scheme (2015) attempted to reduce physical gold imports and remain partial answers.

The third is the inflation-targeting-mandate thread. The RBI's primary mandate under the RBI Act, 1934 (amended 2016) is inflation targeting at 4 per cent (+/- 2) for headline CPI. Currency stability is a secondary consideration; the rupee defence must not compromise the inflation mandate. Governor Sanjay Malhotra's orderly framing preserves the primacy of the inflation target.

UPSC Relevance

Where the rupee episode sits in the UPSC syllabus

UPSC context: The rupee depreciation falls within General Studies Paper III under Indian Economy and issues relating to planning, mobilization of resources, growth, development, effects of liberalization on the economy, and government budgeting. The external-sector dimension also touches infrastructure through the import dependence on crude oil.

Prelims relevance: The Prelims surface includes the managed-float exchange-rate regime, the Real Effective Exchange Rate (REER), the Forward Premium, Forex Reserves components (foreign-currency assets, gold, SDRs, IMF reserve position), the Foreign Exchange Management Act, 1999 (FEMA), the Liberalised Remittance Scheme, FCNR-B deposits, the Monetary Policy Committee structure under the RBI Act, 1934 (amended 2016), and the 4 per cent (+/- 2) inflation-targeting mandate.

Mains relevance: Two framings dominate the Mains-paper surface:

- (i) Protectionism-and-currency-manipulation framing. How protectionism and currency manipulations affect Indian macroeconomic stability. The May 2026 episode is the most current evidence of the US-tariff-pressure channel and the RBI’s orderly-intervention response.

- (ii) Balance-of-payments-and-external-rupee-value framing. Pressures on the balance of payments and the external value of the rupee. The May 2026 record low near 96.96 per USD and the 7.04 per cent YTD depreciation are the headline evidence the question asks for.

Mains practice question: A focused fifteen-mark question would read: The Indian rupee touched a record low near 96.96 per US dollar on 20 May 2026 amidst a 7.04 per cent year-to-date depreciation. Examine the structural and cyclical drivers of the depreciation and discuss the RBI policy stack available for an orderly market response.

- Past Mains linkage. 2018 GS-III: How would the recent phenomena of protectionism and currency manipulations in world trade affect macroeconomic stability of India? The May 2026 episode is the most current evidence the answer must include.

- Past Mains linkage. 2015 GS-III: Craze for gold in India has led to a surge in the import of gold in recent years and put pressure on balance of payments and external value of the rupee. In view of this, examine the merits of the Gold Monetization scheme. The May 2026 rupee fall extends the same balance-of-payments concern the 2015 question framed.

- Prelims linkage. Prelims questions on FEMA, REER, the MPC, and CAD components test the institutional surface.

Prelims MCQ practice

Each question below tests one specific concept on the topic. Click to reveal the answer and a full option-wise explanation.

Q1. With reference to India's exchange-rate regime, consider the following statements:

- India operates a managed-float exchange-rate regime in which the Reserve Bank of India intervenes to smooth volatility.

- Under a managed-float regime, the central bank targets a specific exchange rate level.

- The Real Effective Exchange Rate (REER) is a trade-weighted index of the rupee against a basket of currencies.

Which of the statements given above is/are correct?

- 1 only

- 1 and 3 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1 and 3 only

Explanation.

Statement 1 is correct. India operates a managed-float exchange-rate regime in which the RBI intervenes to smooth volatility while allowing the market to discover the level. Statement 2 is incorrect. Under a managed-float regime, the central bank does NOT target a specific exchange rate level; it smooths volatility around market-discovered levels. The fixed-rate or pegged regime targets a specific level. Statement 3 is correct. The Real Effective Exchange Rate (REER) is a trade-weighted index of the rupee against a basket of currencies, calculated by the RBI on a 40-currency basis. Hence option (b).

Q2. With reference to India's foreign exchange reserves, consider the following statements:

- Foreign Currency Assets (FCA) form the largest component of India's forex reserves.

- Gold reserves form a part of India's foreign exchange reserves.

- Special Drawing Rights (SDRs) of the IMF are included in India's reserves.

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1, 2, and 3

Explanation.

Statement 1 is correct. Foreign Currency Assets (FCA) form the largest component of India's forex reserves, typically over 85 per cent of the total. Statement 2 is correct. Gold reserves form a part of India's foreign exchange reserves, with the holding around 800 tonnes. Statement 3 is correct. Special Drawing Rights (SDRs) of the IMF and the Reserve Tranche Position with the IMF are both included in India's forex reserves. All three statements are accurate, hence option (d).

Q3. With reference to the Foreign Exchange Management Act (FEMA), 1999, consider the following statements:

- It replaced the Foreign Exchange Regulation Act (FERA), 1973.

- It treats violations as civil offences rather than criminal offences.

- It is administered by the Securities and Exchange Board of India (SEBI).

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1 and 2 only

Explanation.

Statement 1 is correct. FEMA, 1999 replaced the Foreign Exchange Regulation Act (FERA), 1973 and came into force on 1 June 2000. Statement 2 is correct. FEMA treats violations as civil offences (with monetary penalties) rather than criminal offences as FERA did. Statement 3 is incorrect. FEMA is administered by the Reserve Bank of India (RBI) under the overall supervision of the Ministry of Finance, not by SEBI. SEBI regulates securities markets, not foreign exchange transactions. Hence option (b).

Q4. With reference to the Monetary Policy Committee (MPC) of the Reserve Bank of India, consider the following statements:

- The MPC was constituted under the Reserve Bank of India Act, 1934 as amended in 2016.

- It is responsible for fixing the policy rate to achieve the inflation target.

- It has six members, three from the RBI and three nominated by the Central Government.

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1, 2, and 3

Explanation.

Statement 1 is correct. The MPC was constituted under the Reserve Bank of India Act, 1934 as amended by the Finance Act, 2016, which introduced the inflation-targeting framework. Statement 2 is correct. The MPC is responsible for fixing the policy rate (the repo rate) required to achieve the inflation target. Statement 3 is correct. The MPC has six members: three from the RBI (Governor as Chairperson, Deputy Governor in charge of monetary policy, and one officer nominated by the Central Board) and three external members nominated by the Central Government. All three statements are accurate, hence option (d).

Q5. With reference to India's inflation-targeting framework, consider the following statements:

- The inflation target is set by the Central Government in consultation with the Reserve Bank of India.

- The current target is 4 per cent CPI inflation with a tolerance band of 2 percentage points on either side.

- If inflation breaches the band for three consecutive quarters, the RBI must submit a report to Parliament.

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1 and 2 only

Explanation.

Statement 1 is correct. The inflation target is set by the Central Government in consultation with the RBI, under Section 45ZA of the RBI Act. Statement 2 is correct. The current target is 4 per cent CPI inflation with a tolerance band of (+/-) 2 percentage points (i.e., 2 to 6 per cent), set for the period 1 April 2021 to 31 March 2026 and continued thereafter. Statement 3 is incorrect. If inflation breaches the band for three consecutive QUARTERS, the RBI must submit a report to the Central Government (not Parliament directly), explaining the reasons, remedial actions, and the expected time-horizon for return to target. Hence option (b).

Q6. With reference to the current account of India's balance of payments, consider the following statements:

- Goods trade deficit is the largest sub-component of the current account.

- Software services exports contribute to the services-account surplus.

- Remittances from overseas Indians are recorded in the capital account.

Which of the statements given above is/are correct?

- 1 only

- 1 and 2 only

- 2 and 3 only

- 1, 2, and 3

Show answer and explanation

Answer: 1 and 2 only

Explanation.

Statement 1 is correct. The goods (merchandise) trade deficit is the largest sub-component of the current account and is the binding constraint that drives the overall current account deficit. Statement 2 is correct. Software and IT-services exports contribute to the services-account surplus, partially offsetting the goods trade deficit. Statement 3 is incorrect. Remittances from overseas Indians are recorded under SECONDARY INCOME (private transfers) in the CURRENT ACCOUNT, not the capital account. Capital account records investment flows (FDI, FPI, ECBs), not remittances. Hence option (b).

Sources

- Reserve Bank of India: Weekly Statistical Supplement

- Ministry of Finance: Economic Affairs department briefings

- Trading Economics: USD/INR historical series

- Ministry of Commerce and Industry: Foreign Trade Policy 2023 and trade data

- Securities and Exchange Board of India: FPI flow data

- Press Information Bureau: RBI Governor statements

- FEMA, 1999 (consolidated text)

- Wikipedia: Foreign Exchange Reserves of India

Editorial Disclaimer

This article is compiled from the reference materials listed in the Sources section. It is an explainer for UPSC preparation and is not a substitute for primary documents (NCERTs, GoI ministry releases, IMD bulletins, RBI / CEA / MoEFCC publications, and Standing-Committee reports).