Overview

Previous Year UPSC-CSE Questions By the end you will be able to draft model answers for the following UPSC questions. Each question carries a collapsible framework showing how to approach it in the exam.

- UPSC Mains 2019 GS-IIIEnumerate the indirect taxes which have been subsumed in the Goods and Services Tax (GST) in India. Also, comment on the revenue implications of the GST introduced in India since July 2017.

How to structure the answer in the exam

Introduction: Open with GST as a unifying reform of indirect taxes from July 2017.

Body (sub-themes to develop):

- Taxes subsumed: excise, service tax, VAT, and several state levies.

- Revenue implications: buoyancy, collections and compensation.

- Simplification and a common national market.

- Continuing issues such as rate rationalisation.

- The parallel direct-tax simplification under the 2025 Act.

Conclusion: Conclude that both GST and the new direct-tax law aim at a simpler, more compliant tax system.

- UPSC Prelims 2018With reference to India's decision to levy an equalization tax of 6% on online advertisement services offered by non-resident entities, consider the following statements:

- It is introduced as a part of the Income Tax Act.

- Non-resident entities that offer advertisement services in India can claim a tax credit in their home country under the 'Double Taxation Avoidance Agreements'.

Select the correct answer using the code given below:

How to approach this Prelims question

Approach: Test each statement against how the equalisation levy is actually designed.

Trap to watch: The equalisation levy was introduced through a Finance Act as a separate levy, not within the Income Tax Act, and it does not qualify for tax credit under double-taxation treaties, so neither statement holds.

Key facts to recall:

- The equalisation levy is a separate levy, not part of the Income Tax Act.

- It is not income tax, so double-taxation treaty credit does not apply.

- It targets certain digital services by non-resident entities.

Answer signal: Both statements are wrong. Correct answer: Neither 1 nor 2.

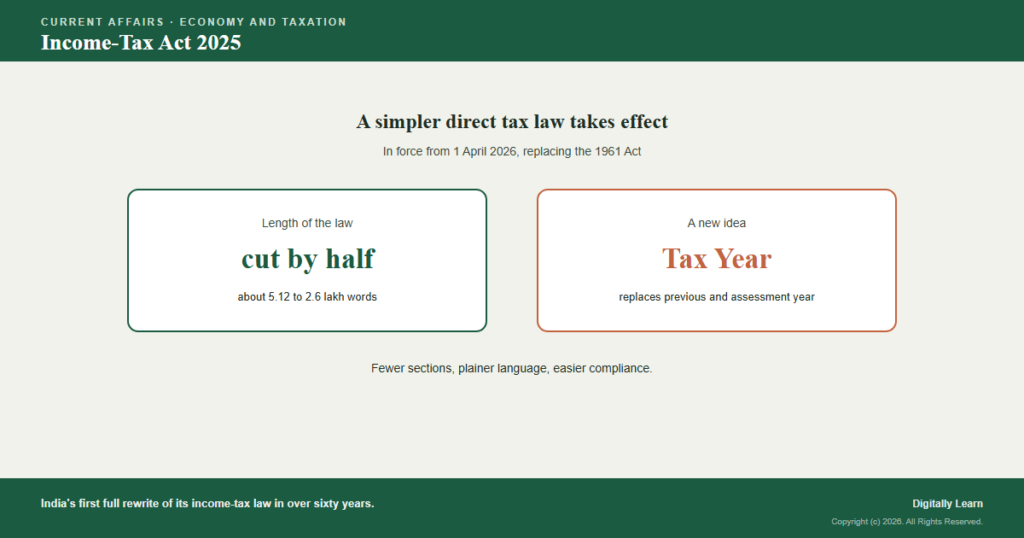

The Income-Tax Act, 2025 is India's new direct tax law, which came into force on 1 April 2026. It replaces the Income-tax Act, 1961, which had grown complex through decades of amendments. Passed by Parliament in August 2025, the new Act keeps the tax rates and policy broadly unchanged but rewrites the law in plain, simpler language. It cuts the text roughly in half, reduces the number of sections and chapters, and introduces a single Tax Year in place of the old previous year and assessment year. The aim is easier compliance and less litigation.

Why the new income-tax law is in focus

A full rewrite of India's income-tax law

The Income-Tax Act, 2025 came into force on 1 April 2026. It replaces the Income-tax Act of 1961, which had governed direct taxation in India for more than six decades.

A direct tax is one paid directly to the government by the person or firm on whom it falls, such as income tax. The new Act is the statute that sets out how income is taxed in India.

The Act was passed by Parliament in August 2025 and received the President's assent on 21 August 2025. It is a simplification, not a change of tax rates, rewriting the old law in plainer language.

The key features of the new Act are:

- Replacement: it supersedes the Income-tax Act of 1961.

- Shorter text: the law is cut from about 5.12 lakh to 2.6 lakh words.

- Fewer parts: the number of sections and chapters has been reduced.

- Tax Year: a single Tax Year replaces the previous year and assessment year.

Why the new Act matters

Simpler law, easier compliance

The old 1961 Act had become dense and hard to read after hundreds of amendments. A clearer law lowers the cost of understanding tax rules for ordinary taxpayers and businesses alike.

The text has been cut from about 5.12 lakh words to 2.6 lakh words, with fewer sections and chapters, so the same policy is now expressed in roughly half the space.

It also matters for litigation. Plainer drafting, with tables and formulas in place of dense text, is meant to reduce ambiguity, fewer disputes, and so ease the burden on taxpayers and courts.

What the new Act signifies

Continuity of policy, clarity of form, ease of use

Three threads carry the weight: continuity of tax policy, a clearer structure, and a focus on the taxpayer's ease of use.

First, continuity of policy. The Act keeps tax rates and the broad policy intact, so the change is about how the law reads, not about how much tax people pay.

Second, a clearer structure. The number of chapters and sections has been cut, and dense provisions are recast using tables and formulas, making the law easier to navigate.

Third, ease of use. The single Tax Year removes a long-standing source of confusion, and simplified forms are meant to make filing returns more straightforward.

Distinguishing features of the new Act

The Act at a glance

The table sets the old law against the new one, so the scale of the simplification is visible at a glance.

| Feature | Income-tax Act 1961 | Income-Tax Act 2025 |

|---|---|---|

| Word count | About 5.12 lakh | About 2.6 lakh |

| Chapters | 47 | 23 |

| Sections | 819 | 536 |

| Key time concept | Previous year and assessment year | Single Tax Year |

Three features that define the Act

Three elements set the 2025 Act apart from the old 1961 law:

- (i) The Tax Year. A single twelve-month Tax Year replaces the confusing previous year and assessment year pair.

- (ii) Tables and formulas. Dense legal text is recast using dozens of tables and formulas for clarity.

- (iii) Consolidation. Scattered provisions are grouped, for example tax deducted at source is brought under one section.

Observable outcomes

Three trackable outcomes

The new Act translates into three developments to watch as it beds in.

- (a) New rules and forms. The tax authority is notifying fresh rules and simplified forms to match the Act.

- (b) Taxpayer outreach. Awareness drives are helping taxpayers and professionals adjust to the new structure.

- (c) Fewer disputes, in time. The test of the reform is whether clearer drafting actually lowers tax litigation.

A simpler law is a start, not a guarantee. Smooth transition depends on clear rules, good systems and how courts read the new provisions.

The Act, the transition and tax reform

Which law applies when, and the wider reform

The change involves a careful transition. Income earned in the financial year 2025-26 is still governed by the old 1961 Act, while income from 1 April 2026 falls under the new Act.

It fits a wider drive for tax reform and ease of doing business, alongside earlier steps such as faceless assessment and the simplification of the indirect-tax system through the Goods and Services Tax.

It also rests on the work of the Central Board of Direct Taxes, the body under the Finance Ministry that administers direct taxes and is issuing the rules and forms for the new Act.

UPSC relevance and exam focus

Where this fits in the UPSC-CSE syllabus

This topic maps to General Studies Paper III: Indian economy, mobilization of resources, and government budgeting, with links to governance reform in Paper II.

For Prelims, hold the high-yield facts: the new Act replaces the 1961 law, came into force on 1 April 2026, and introduces the single Tax Year concept.

For Mains, two framings recur: tax simplification as a tool for compliance and growth, and the difference between direct and indirect tax reform.

Recurring linked concepts an aspirant should keep in working memory:

- Direct tax: a tax paid directly to the government, such as income tax.

- Tax Year: the single twelve-month period in the new Act.

- CBDT: the Central Board of Direct Taxes, which administers direct taxes.

- Faceless assessment: an earlier reform to reduce direct contact in tax scrutiny.

The new Act simplifies the law; it does not, by itself, change the tax rates. Assuming a rate change is a frequent error.

Do not confuse this direct-tax reform with the Goods and Services Tax. The GST overhauled indirect taxes, while this Act rewrites the income-tax law.

Prelims MCQ practice

Each question below tests one specific concept on the topic. Click to reveal the answer and a full option-wise explanation.

Q1. Consider the following statements regarding the Income-Tax Act, 2025:

- It came into force on 1 April 2026.

- It replaces the Income-tax Act of 1961.

- It introduces a single Tax Year concept.

Which of the statements given above is/are correct?

- 1 and 2 only

- 2 and 3 only

- 1 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1, 2 and 3

Explanation.

All three are correct. The Income-Tax Act 2025 came into force on 1 April 2026, replaces the 1961 Act, and introduces the single Tax Year. Hence 1, 2 and 3.

Q2. The 'Tax Year' introduced by the new Act replaces which one of the following pairs of terms?

- Financial year and calendar year

- Previous year and assessment year

- Fiscal year and accounting year

- Base year and reference year

Show answer and explanation

Answer: Previous year and assessment year

Explanation.

Option (b) is correct. The single Tax Year replaces the previous year and assessment year of the 1961 Act, which often confused taxpayers. The other pairs are not the terms it replaces. Hence option (b).

Q3. The Income-Tax Act, 2025 primarily reforms which category of taxation?

- Indirect taxation

- Direct taxation

- Customs duties

- Goods and Services Tax

Show answer and explanation

Answer: Direct taxation

Explanation.

Option (b) is correct. Income tax is a direct tax, so the new Act reforms direct taxation. Customs and GST are indirect taxes, governed by separate laws. Hence option (b).

Q4. Consider the following statements about the new Act:

- It significantly shortens the text of the income-tax law.

- It changes the basic income-tax rates as its main purpose.

- It uses tables and formulas to simplify provisions.

Which of the statements given above is/are correct?

- 1 and 2 only

- 1 and 3 only

- 2 and 3 only

- 1, 2 and 3

Show answer and explanation

Answer: 1 and 3 only

Explanation.

Statements 1 and 3 are correct: the Act shortens the text and uses tables and formulas. Statement 2 is wrong, because its main purpose is simplification, not changing tax rates. Hence 1 and 3 only.

Q5. Which body, under the Ministry of Finance, administers direct taxes and is issuing the rules for the new Act?

- The Reserve Bank of India

- The Central Board of Direct Taxes

- The Central Board of Indirect Taxes and Customs

- The Securities and Exchange Board of India

Show answer and explanation

Answer: The Central Board of Direct Taxes

Explanation.

Option (b) is correct. The Central Board of Direct Taxes administers direct taxes and frames the rules and forms. The CBIC handles indirect taxes, while the RBI and SEBI are the monetary and securities regulators. Hence option (b).

Q6. Under the transition, income earned in the financial year 2025-26 is governed by which law?

- The Income-Tax Act, 2025

- The Income-tax Act, 1961

- Neither, as it is tax-exempt

- Both Acts equally

Show answer and explanation

Answer: The Income-tax Act, 1961

Explanation.

Option (b) is correct. Income of the financial year 2025-26 is still assessed under the old 1961 Act; only income from 1 April 2026 falls under the 2025 Act. Hence option (b).

Sources and Further Reading

- Income Tax Department: Income-tax Act, 2025 comes into force from 1 April 2026 (press release)

- Press Information Bureau: Income-tax Act, 2025 comes into force from today (1 April 2026)

- Income Tax Department: Income-tax Act, 2025

- Press Information Bureau: The Income Tax Act 2025 to come into effect from 1 April 2026

- Ministry of Finance, Department of Revenue

- Wikipedia: Income-tax Act, 2025

Editorial Disclaimer

This article is compiled from the reference materials listed in the Sources section. It is an explainer for UPSC preparation and is not a substitute for primary documents (NCERTs, GoI ministry releases, IMD bulletins, RBI / CEA / MoEFCC publications, and Standing-Committee reports).